Originally published by Analysys Mason. Read the original article here.

“Digital assets are shifting towards private markets, while public markets show growing interest in space platforms. Diverging valuations create opportunities to unlock value through better matchmaking between platform and capital.”

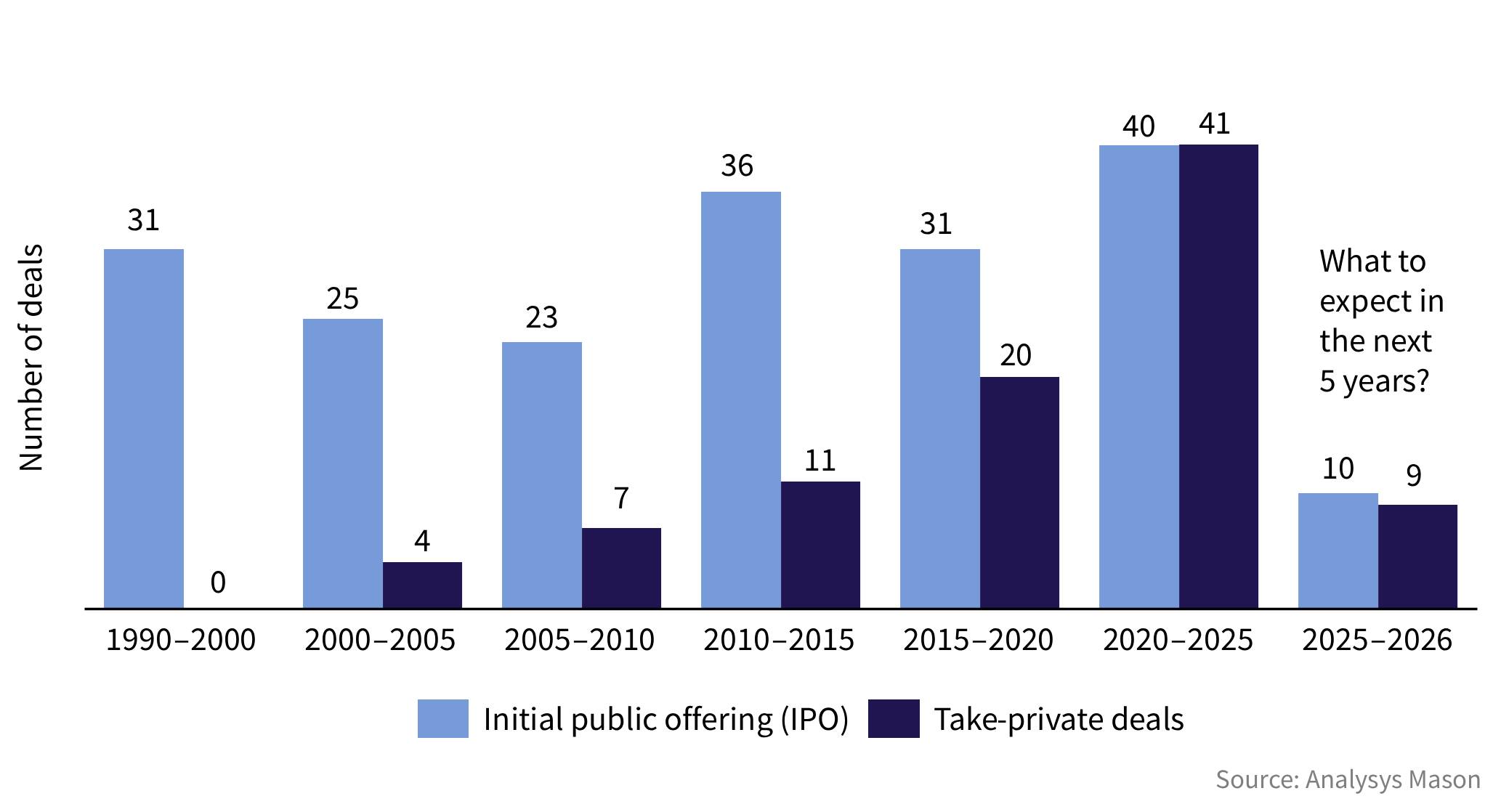

Since Analysys Mason first published IPOs versus take-private: a look back at 120 deals in the telecoms and digital infrastructure sector in August 2025, we have expanded our database of IPO and take-private deals by both volume and sector coverage. The database now includes around 288 deals from 1990 to 2026 across data centres, space, telecoms, fixed infrastructure, wireless infrastructure and technology; 196 of these are IPOs and 92 are take-private deals.

Our previous analysis showed that take-private deals had begun to outpace IPOs. The expanded dataset continues to support this trend.

Figure 1: The number of deals in the telecoms, space and digital infrastructure sectors

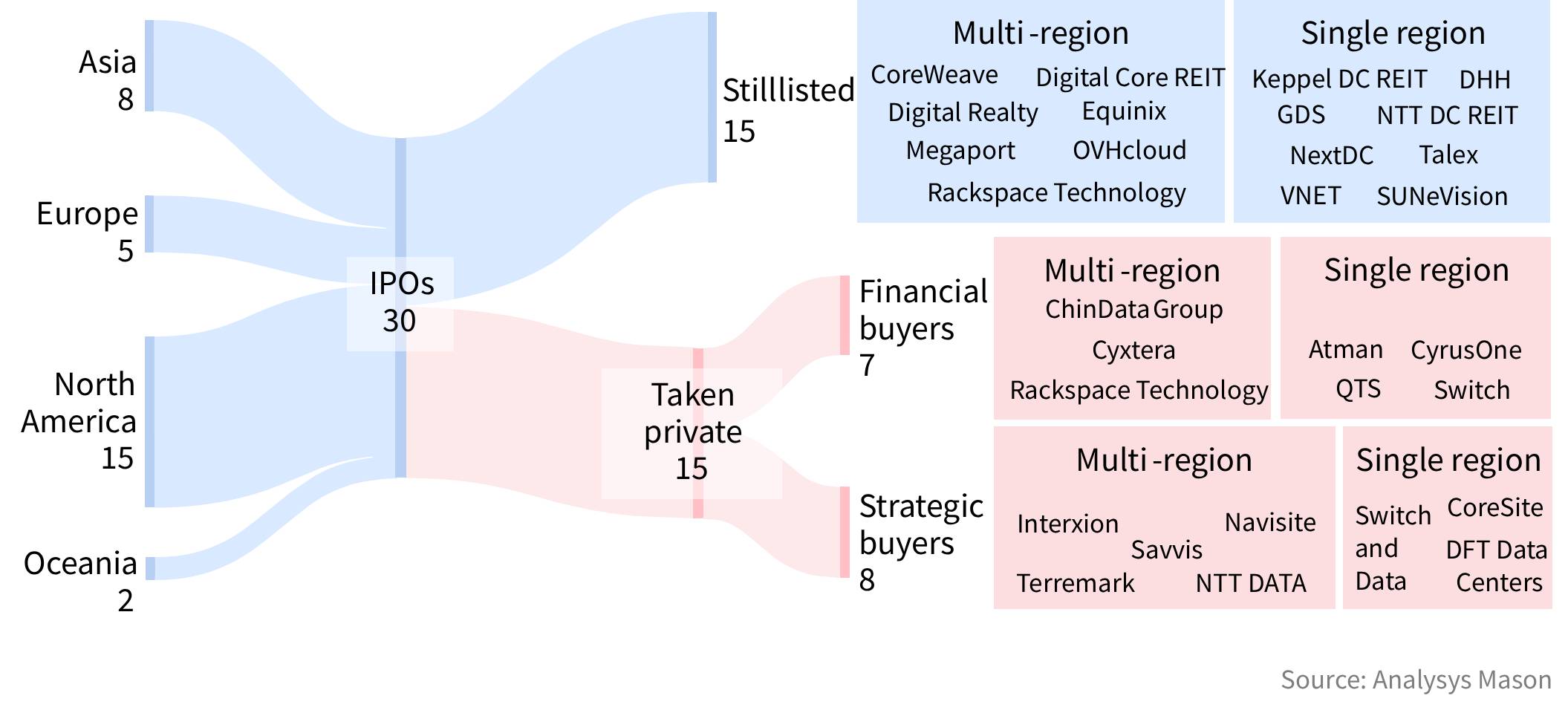

This trend is particularly evident in mature digital infrastructure markets, especially data centres, where more than half of the listed platforms in our dataset have recently been taken private.

Figure 2: Evolution of IPOs and take-private deals in the data centre market

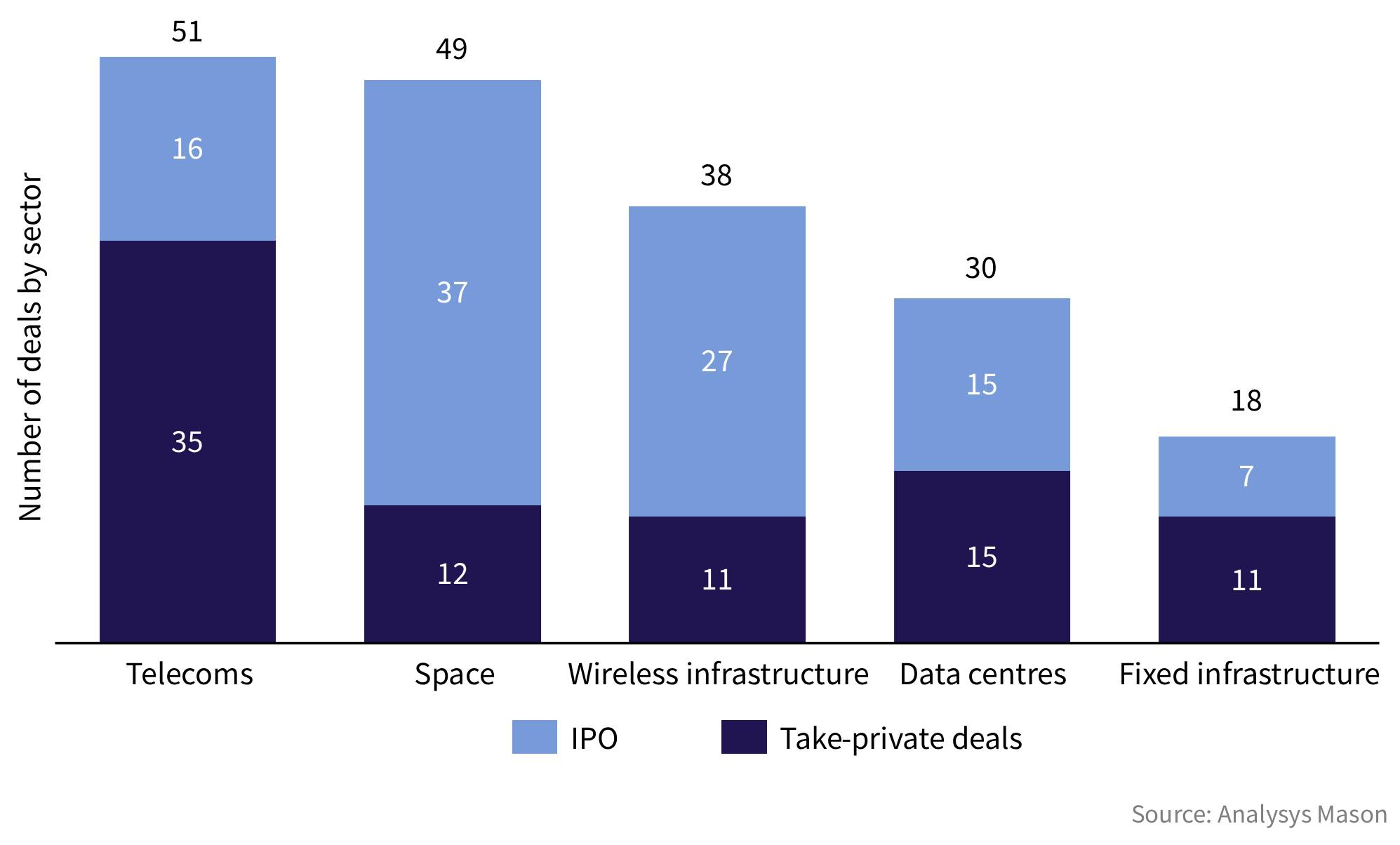

The shift towards take-private deals is clearer in the more mature telecoms and digital infrastructure verticals, although continued IPO activity in the space economy makes the overall trend appear less pronounced.

Figure 3: Number of IPOs and take-private deals by sector, 1990–2026

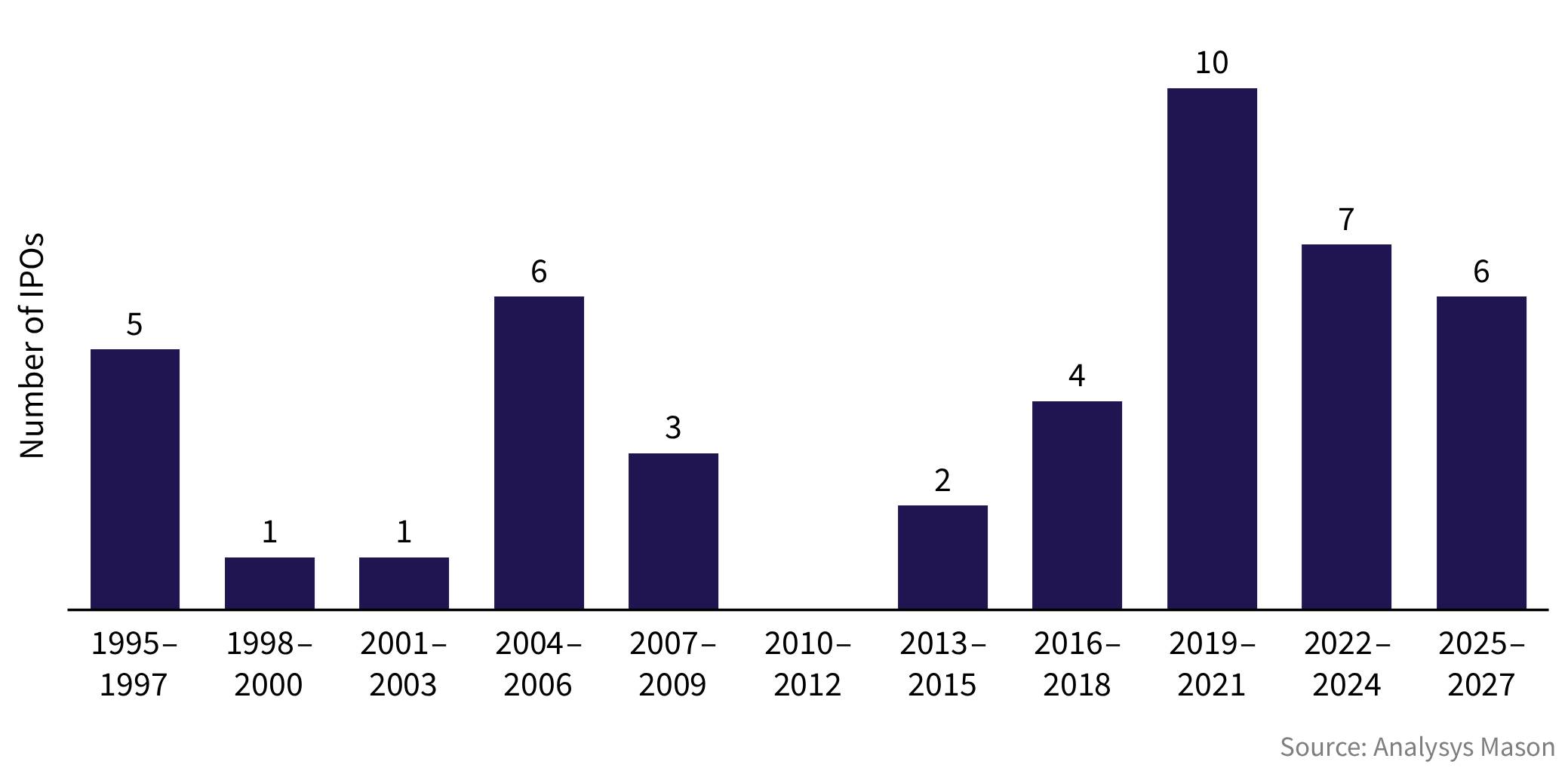

The SpaceX IPO is only the tip of the iceberg: Analysys Mason has tracked around 37 space IPOs in the past 10 years.

Figure 4: Number of space IPOs worldwide, 1995–2026

What this means for investors

Private investors are likely to continue monitoring opportunities to take listed platforms private in more mature digital infrastructure and telecoms operator verticals. These opportunities may arise where public market valuations do not fully reflect a platform’s long-term growth potential, creating scope for private investors to unlock value over a longer investment horizon.

Public markets, by contrast, offer liquidity that can support early-stage growth companies. This makes them particularly relevant for innovative sectors such as space, where companies often need access to capital to scale quickly while their business models are still maturing.

Originally published by Analysys Mason. Read the original article here.