The Middle East’s space sector is undergoing a profound transformation. Once limited to purchasing satellite telecommunications and Earth observation systems from foreign sources, the region now views space as a strategic pillar for economic diversification, national security, and technological sovereignty. This revolution is driven by a convergence of factors: the urgency to move beyond hydrocarbon-dependent economies, the need to guarantee sovereign capabilities in an era of increased geopolitical competition and the desire to project soft power on the world stage.

After a decade of a start-up phase devoted to laying the political, financial and industrial foundations, the region’s space sector is entering a new era of maturity. This new phase of development integrates local and global dynamics, prioritizing innovation and the growth of a self-sustaining ecosystem capable of playing a leading role in the global space industry.

Space Responds to Strategic Imperatives

Volatility and transitions in energy markets have prompted Gulf countries to seek other drivers of economic growth. The space sector, with its potential to stimulate innovation, create highly skilled jobs and attract foreign investment, has become a key part of their diversification strategy. Countries such as the UAE, Saudi Arabia and Egypt are investing in space not only as a technological enabler, but also, and above all, as an economic catalyst.

The multiplier effects of the sector, which stimulates industries such as advanced manufacturing, AI and data analytics, contribute to fulfilling broader national visions, such as the UAE’s Centennial 2071, Oman’s Vision 2040 and Saudi Arabia’s Vision 2030. By encouraging the development of a national space industry, Middle East countries aim to reduce their reliance on foreign expertise, build and retain national intellectual property and capture a share of the global space economy, estimated at $596 billion in 2024.

The Middle East stands at the heart of a reshaped geopolitical landscape marked by escalating security tensions. These challenges have brought defense and security imperatives to the forefront, leading to a sharp increase in military investment ($243 billion in 2024 according to SIPRI, a 19% growth over 10 years), including for space. Independent border surveillance, tracking enemies and securing infrastructure are essential in a region where alliances are fluid and threats are asymmetric, making sovereign space capabilities a key strategic asset.

Space is also a powerful tool for soft power. High-profile missions such as the UAE’s Hope Probe to Mars, Saudi Arabia’s astronaut program and Turkey’s lunar ambitions signal elevated ambitions for national global standing. These initiatives project an image of innovation and forward-thinking leadership.

Investment in Space: Surge, Gaps and New Realities

In just 20 years, the Middle East has evolved from a secondary player in the global space industry into a key financial hub. Institutional and private stakeholders worldwide now view the region, and particularly the GCC countries, as key partners, thanks to their unmatched investment capacity. With the region’s sovereign wealth funds managing cumulative assets exceeding $3 trillion, the region has become a prime destination for players in the space industry, especially NewSpace companies that are scaling up and facing funding limitations in their home markets.

Sovereign wealth funds in the Middle East, particularly Saudi Arabia’s Public Investment Fund (PIF) and the UAE’s Mubadala, have identified space as a top-tier investment domain, aligning with their national ambitions in the sector. However, despite this high-level prioritization, these funds have so far adopted a rather measured approach to direct investments in space ventures. The caution stems from a perceived mismatch between the funds’ investment criteria and the profile of typical space start-ups in terms of risk, deal size and scalability compared to their corporate standards.

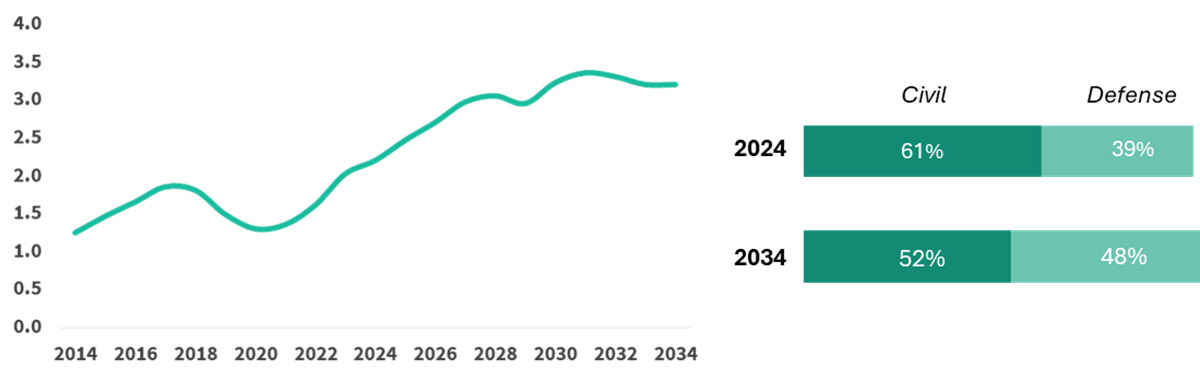

Meanwhile, governments’ financial commitment to space in the region has increased substantially. Space budgets in the Middle East and North Africa (MENA) have gone up by 69% in 10 years, from $1.4 billion (2015) to $2.5 billion (2025). This growth is expected to continue, with spending reaching $3.2 billion by 2034 (+30% over 2025) illustrating strong commitments from governments in the region to develop space capabilities and grow their sector, with a strong push towards defense and security.

Still, the gap with established space nations remains huge:

- MENA countries account for just 1.8% of global government space investments, compared to 59% for the United States and 13% for Europe.

- As a share of regional GDP, space spending in the region stands only at a low (but growing) level of 0.05%, while the U.S. allocates 0.25% and Europe 0.1%. Therefore, there is much room for normalizing the region’s investment to global standards.

Space is not only expensive, its cost is rising. To ensure a meaningful role on the global stage, countries must commit to high funding in the context of an investment race between leading nations. This challenge will inevitably strain resources that only the most financially robust countries will be able to sustain over the long term. In the region, this dynamic risks widening the gap between countries capable of supporting financially ambitious space programs and those likely forced to revise their strategies due to budgetary constraints.

MENA Governments Allocations to Space Activities (US$B)

As the ecosystem matures, governments are allocating resources to more advanced and strategic domains:

- Space Exploration: Missions to the Moon, Mars and beyond are no longer the exclusive domain of historical space nations. The UAE’s Hope Probe, Turkey’s AYAP Lunar Program and Saudi Arabia’s astronaut missions signal a new era of exploration.

- Access to Space: The region is investing in launch capabilities, with countries exploring partnerships to develop sovereign launch sites (e.g. Oman) or to invest into launch ventures (e.g. UAE, Saudi Arabia, Turkey).

- Defense and Security: The demand for military satellites, remote sensing systems and secure communications is driving investments in dual-use technologies.

- Commercial Space: Governments are incentivizing private-sector participation through funds, incubators and public-private partnerships, mirroring the global NewSpace trend.

Normalized Governance and Regulation

The rise of the space sector in the Middle East has come with structural reforms aimed at aligning local governance with international standards. Historically, space activities in the region were managed on an ad hoc basis, often fragmented across multiple ministries, with little coordination or strategic oversight. Today, countries are centralizing space governance by creating dedicated space agencies and councils, modelled on frameworks used in leading space nations.

- Saudi Arabia and the United Arab Emirates have created space councils to streamline national visions, set priorities, and coordinate cross-sector efforts.

- Turkey has created its space command to oversee military space activities, reflecting a broader trend toward institutional consolidation.

As the private sector plays an increasingly important role, governments have also developed regulatory frameworks in line with global best practices. Countries such as the UAE, Saudi Arabia and Egypt have implemented comprehensive regulations to govern commercial space activities, and many others are following suit. These reforms aim to strike a balance between innovation and oversight, ensuring that private companies can thrive while remaining aligned with national strategic objectives. As a result, the Middle East is rapidly becoming one of the most advanced regions in terms of space regulation, positioning itself as a hub for innovation and responsible governance.

Localization and Consolidation to Reduce Dependence

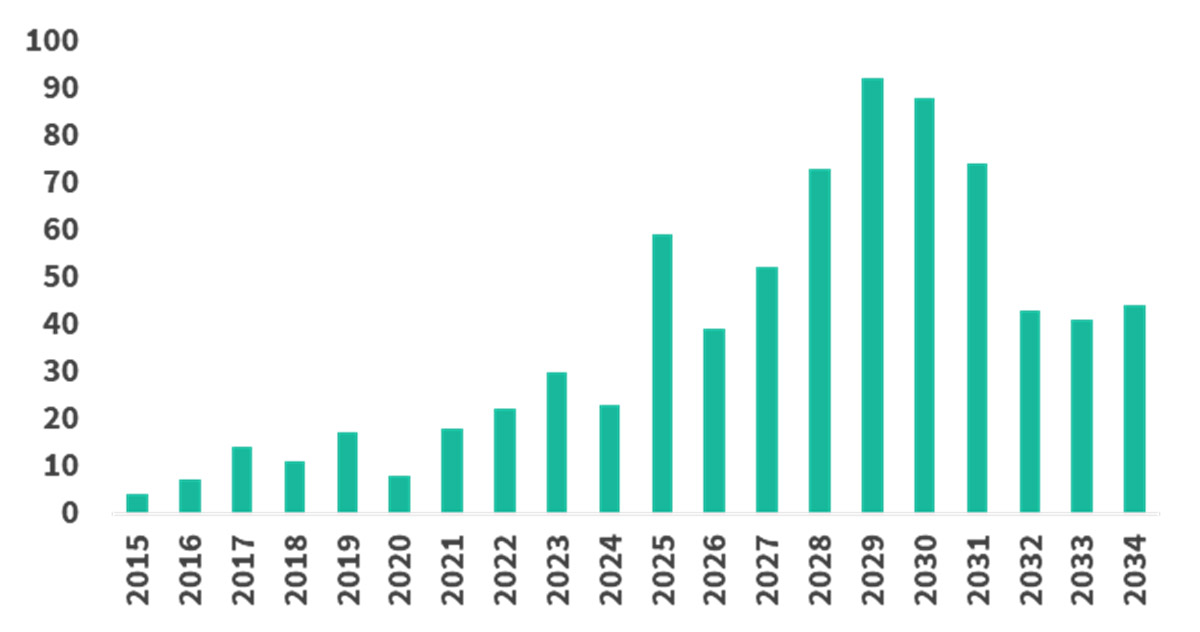

The intensification of space activities in the Middle East is exemplified by satellite procurement from government and commercial entities. Having launched approximately 150 satellites over the past decade, regional players are now set to acquire and deploy more than 600 satellites over the next decade, underscoring significant growth and diversification in locally operated space assets.

Besides, a defining feature of the Middle East’s space maturation is the shift from assumed dependency to localization of space capabilities. Historically, countries in the region depended on foreign suppliers for their space infrastructure and services. Today, many are designing, manufacturing, and operating their own space assets. As an illustration:

- The UAE’s MBZ-SAT was 90% manufactured locally.

- Egypt’s NexSat program aims for a 60% local contribution to its microsatellites.

- Turkey’s Göktürk-3 satellite is fully developed and produced in the country.

Satellites Launched by MENA Operators (all types)

This localization is not just about technological sovereignty: it is coupled with an integrated industrial vision. Previously, the Middle East’s space ecosystem was dominated by subsidiaries of international companies. Today, the region is cultivating its own national champions, often formed from new conglomerates adopting a vertically integrated model, in which they control multiple segments of the value chain, from space infrastructure to services.

- Space42 (UAE) combines Yahsat’s satellite communications with Bayanat’s geospatial analytics and AI, creating a one-stop shop for space services.

- Neo Space Group (Saudi Arabia) aims to integrate space systems and services through domestic and international acquisitions (e.g. Taqnia Space, Airbus’s UP42).

- EDGE Group’s FADA (UAE) develops sovereign satellite platforms and is building assembly, integration, and testing (AIT) facilities to localize production.

- Turkey’s Baykar has created Fergani Space as its dedicated venture for space-based solutions with key objective to localize critical space technologies across satellites and orbital infrastructures.

Beyond the emergence of these new national giants, the growth of space ecosystems in the region is also being driven by a wave of space start-ups, supported by public funding, incubators, and a growing pool of local talent.

Several key initiatives illustrate this dynamic. The UAE’s $820 million National Space Fund actively supports infrastructure development, start-up growth, and the creation of international partnerships, thereby strengthening the sector’s competitiveness. In Saudi Arabia, the Madarik program trains participants in space-related jobs, covering fields as diverse as space commerce, engineering and data science, in order to prepare a new generation of skilled professionals. In 2025, the Omani government launched its first space accelerator program aimed at stimulating the development of local industry, in line with its national space strategy. Together, these initiatives are helping to shape an innovative, diverse, and resilient regional space ecosystem.

The Future: A Hub for Space Innovation

The space sector in the Middle East is at a historic turning point. In just a few years, space has evolved from an ambitious vision to a strategic reality for most players in the region. Through bold investments, governance reforms and ecosystem modernization, the region has reached a stage of maturity that positions it as a new global space hub.

The road ahead is not without challenges. Long-term talent development, the creation of a domestic market to reduce dependence on imports and exports and the diversification of local ecosystems are among the complex issues that need to be addressed. Yet the region has key strengths, including its ability to quickly adapt to new realities in the global space sector, while others must realign their historical models. The momentum of space in the Middle East is undeniable and holds great promises for the years to come.

About the Author

Steve Bochinger is an affiliate executive advisor at Novaspace and renowned expert in the space sector with more than 25 years of experience in consulting with government and private space organizations. He also is an associate professor at University Paris-Saclay in space law, economy and policy.