Originally published by Space Intel Report. Read the original article here.

Matt Desch. (Source: Iridium)

Matt Desch. (Source: Iridium)

MOUNTAIN VIEW, Calif.— Iridium Chief Executive Matt Desch has long resisted the temptation to boost his stock by latching on to the latest market fashion.

He was cautious about the potential for direct-to-device (D2D) broadband as a market even as Iridium moved into the narrowband end of it starting this year.

He has not hyped “Golden Dome” as a revenue opportunity on every quarterly call, even though Iridium’s work with the US Space Development Agency on network operations offers Golden Dome-relevant potential.

And he is not falling for space-based data centers, which is almost certainly many years away.

“Valuations in the satellite industry are increasingly being driven by future narratives rather than by current operating results,” Desch said in a Feb. 12 investor call. “As we focus on new growth areas, we recognize the need to broaden, and more clearly articulate, our growth narrative.”

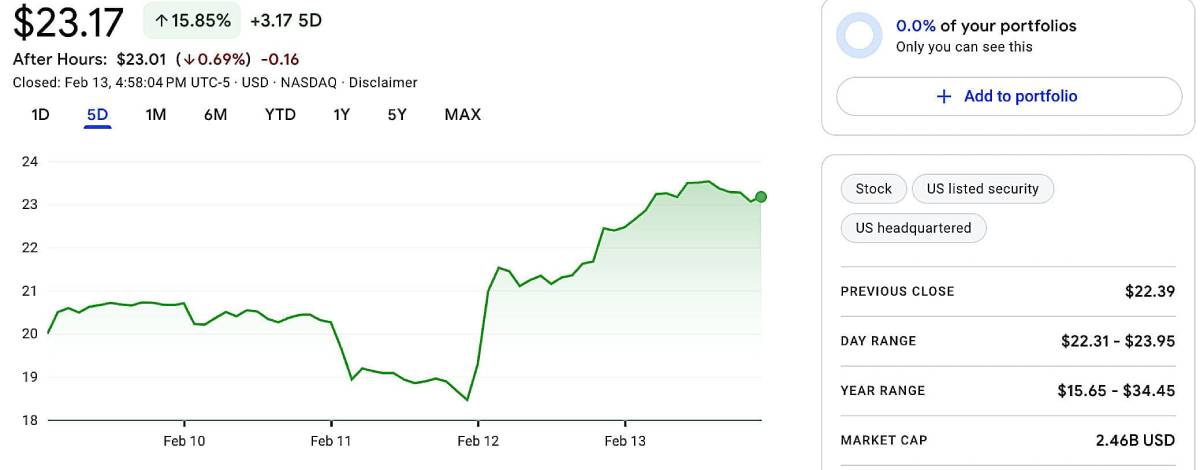

Iridium is doing that. But SpaceX’s $19.6-billion purchase of EchoStar Corp.’s D2D spectrum in late 2025 is stretching the limit of Desch’s ability to resist joining the party.

In a Feb. 12 investor call, Desch acknowledged that the transaction caused investors to reassess Iridium in the negative, on the assumption that this latest SpaceX steamroller would leave Iridium as roadkill.

(Source: Iridium)

(Source: Iridium)

As a company sitting on L-band spectrum whose value is now widely recognized for D2D, and one whose current constellation could easily make room for a partner/investor without disturbing current customers, Iridium now sees no harm in evoking the idea of a transaction — a merger, being the target of an acquisition or a partnership.

“Our spectrum, in and of itself, has great value,” Desch said. “In light of industry developments of recent months and the excitement over the prospects for D2D, MSS spectrum — especially clean, globally coordinated spectrum — has increased in value.

“Therefore, we will not rule out future business alliances to leverage our unique spectrum real estate, particularly if they offer incremental value to shareholders.

“Given the investment that Starlink has made in spectrum, we have seen an increase in industry people talking with each other and positioning themselves for the is D2D market. We are seeing opportunities with people who value our partners and existing businesses and value our unique L-band spectrum position. There is just a lot of discussion and it could go in a lot of different directions.”

(Source: Google Finance)

(Source: Google Finance)

There — he walked onto the dance floor. And he got the pop in his company’s stock.

What Desch really wants to talk about is Iridium’s expected growth in four different areas as it passes through a temporary period of modest results.

Here’s how the company sees these four areas:

(Source: Iridium)

(Source: Iridium)

— Narrowband IoT

Otherwise known as the less-spectacular end of D2D, Iridium’s NTN Direct service, this business builds on Iridium’s successful IoT serve by adding a standards-based service that can find its way into phones, watches, drones and other platforms.

This year the company will introduce it and has started beta testing with partners. The next step will be chipset suppliers agreeing to put the service on their products, and mobile network operators aligning with it for a roaming or unserved-area service for their customers. Expect no real revenue uptick until 2027.

Other companies have L-band spectrum, but few have global spectrum. SpaceX now does with the EchoStar transaction, but AST SpaceMobile is relying on MNOs for its coverage outside the United States. It has an agreement with Ligado Networks for L-band access in the US.

Desch said the Equatys joint venture of Viasat Inc. and UAE-based Space42 both have spectrum but the joint venture’s status is unclear. Viasat has not announced any investment in it; Space42 has.

“This is more long-term and nobody knows when it would happen,” Desch said. It looks like a spectrum condo situation. I don’t know how serious that is. It’s available to use maybe down the road, but that’s many years away and I don’t think it’s relevant.”

Iridium’s IoT subscriber business continues to grow. The company reported 1.998 million subscribers generating $181.4 million in revenue at an average $7.78 in monthly revenue in 2025, compared to $166.2 million in revenue from 1.887 million subscribers in 2024.

(Source: Iridium)

(Source: Iridium)

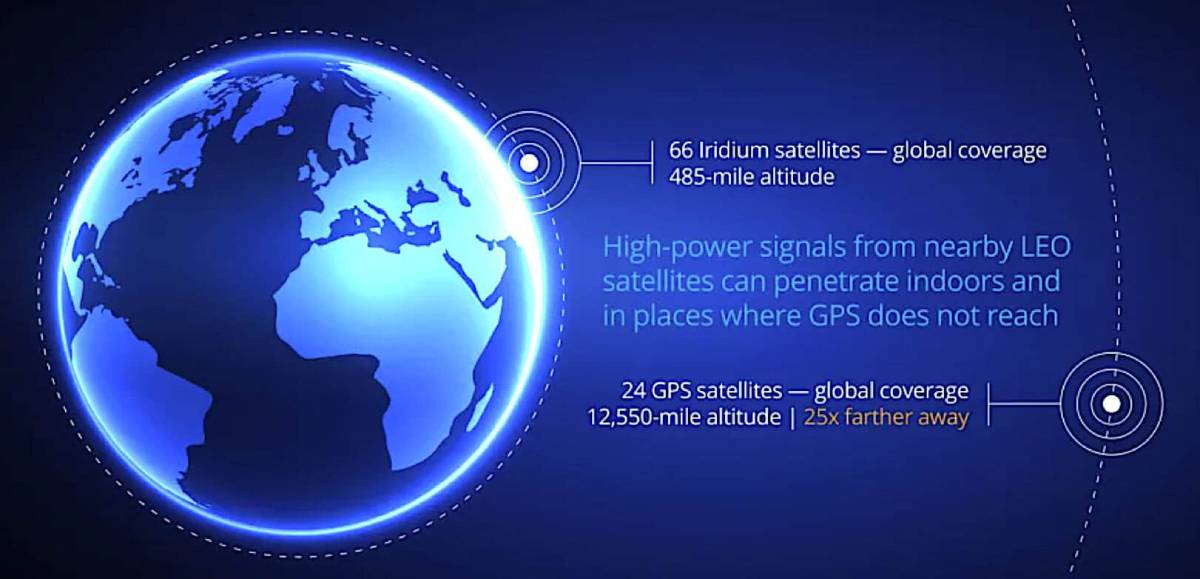

Alternate positioning, navigation and timing

Iridium has been developing an L-band based service using its existing constellation to mitigate the jamming/spoofing effects on Global Navigation Satellite Systems (GNSS) such as the US GPS and Europe’s Galileo.

Iridium PNT offers a signal 1,000 times as strong as GNSS and penetrates indoors. Iridium is among several governments and commercial players planning similar networks. Iridium’s advantage is that it does not need to launch any satellites to begin the service.

Iridium has told investors that its PNT service will generate $100 million in annual revenue by the end of the decade. The company declined to specify 2025 revenue, but Desch said it was “more than” $10 million.

The company will introduce a new chip to its PNT service this year. Desch said requests to take part in the beta testing “far exceeded our expectations.

“With this chip we are at least five years ahead of any competitive PNT solutions,” Desch said. “This hardware will lower installation costs.”

(Source: Iridium)

(Source: Iridium)

Cockpit connectivity and security

Iridium’s ownership stake in Aireon, which uses Iridium’s constellation for an aircraft tracking and monitoring service, offers the company leverage to more fully enter this business. Iridium provides cockpit communications to more than 60,000 aircraft and wants to expand this to drones and other platforms.

Desch said flight-testing with multiple aircraft types has begun with Iridium’s Certus broadband service and this will take several months. By 2027, he said, it should be ready for installation into commercial aircraft.

National security and the US military

The US government has long been Iridium’s biggest customer. Its $738.5-million, seven-year Enhanced Mobile Satellite Services (EMSS) unlimited airtime contract with the US Department of Defense comes to an end this year, but Iridium Chief Financial Officer Vincent J. O’Neill said it’s expected to expects it to be extended by six months, to March 2027, as the two parties negotiate a successor.

(Source: Iridium)

(Source: Iridium)

Iridium values it five-year, $491-million SDA contract, won with General Dynamics Mission Systems, at $239 million. the contract is for the ground management and integration of SDA’s multiple missile-warning/missile-defense constellations.

Iridium sees a near-term opportunity in placing its Certus maritime hardware on ships as part of the Global Maritime Distress and Safety Service (GMDSS), where it would be used as backup for Ka-band broadband connections.

Iridium estimates that some 130,000-140,000 Inmarsat-C terminals are nearing retirement, opening an opportunity to replace them.

Desch said Iridium’s stock was downgraded “around a gut reaction that we couldn’t compete against Starlink long term and that they would come into our traditional areas and that we were going to be a company in decline.

“We are actually still growing, last year and this year and faster in the coming years. We have the assets and the direction to be able to overcome those headwinds and grow at a higher rate than today,” Desch said.

“It’s really about whether you think Iridium is a bet for the future. We think we are.”

Originally published by Space Intel Report. Read the original article here.